How to Set Up a Roth IRA (Step by Step)

A Roth IRA is an individual retirement account that allows after-tax contributions to grow tax-free, with qualified withdrawals in retirement also tax-free. It is available to anyone with earned income below the IRS income limits and is widely considered one of the most tax-efficient long-term investment vehicles for individuals who expect their income or tax rate to increase over time. For 2026, the annual contribution limit is $7,500 ($8,600 if you're 50 or older).

TL;DR

A Roth IRA lets you invest after-tax dollars that grow tax-free and can be withdrawn tax-free in retirement. Open one at Fidelity, Schwab, or Vanguard, it takes about 10 minutes. Choose a low-cost index fund like VOO (S&P 500) or VTI (total U.S. market). The 2026 contribution limit is $7,500 ($8,600 if 50+). That's $625/month to max it out. Set up automatic contributions so the system runs itself. At a 10% average annual return, $625/month for 30 years grows to approximately $1.4 million tax-free in retirement.

The Framework

Choose a brokerage. Fidelity, Schwab, or Vanguard are the most commonly recommended for low fees, broad fund selection, and no account minimums. The differences between them are minor for most investors. Pick one and open the account online — it typically takes 10–15 minutes.

Select "Roth IRA" as the account type. Not a traditional IRA. Not a general brokerage account. When prompted during setup, select Roth IRA specifically. This determines the tax treatment of your contributions and growth.

Pick one index fund. VOO (Vanguard S&P 500 ETF, 0.03% expense ratio), VTI (Vanguard Total U.S. Market ETF, 0.03%), or FXAIX (Fidelity 500 Index Fund, 0.015%). One fund provides broad diversification across hundreds of companies. (Vanguard: VOO overview)

Set up automatic contributions. $625/month maxes the account at $7,500/year. If that's not feasible, start with what you can — $50, $100, $200/month. Automate transfers from your checking account on payday so contributions happen without manual effort.

Leave it alone. This money is for long-term compounding. Historically, the S&P 500 has averaged approximately 10% annual returns over rolling 30-year periods. Checking your balance frequently or reacting to short-term market movements tends to reduce returns, not improve them. (S&P 500 historical returns — Macrotrends)

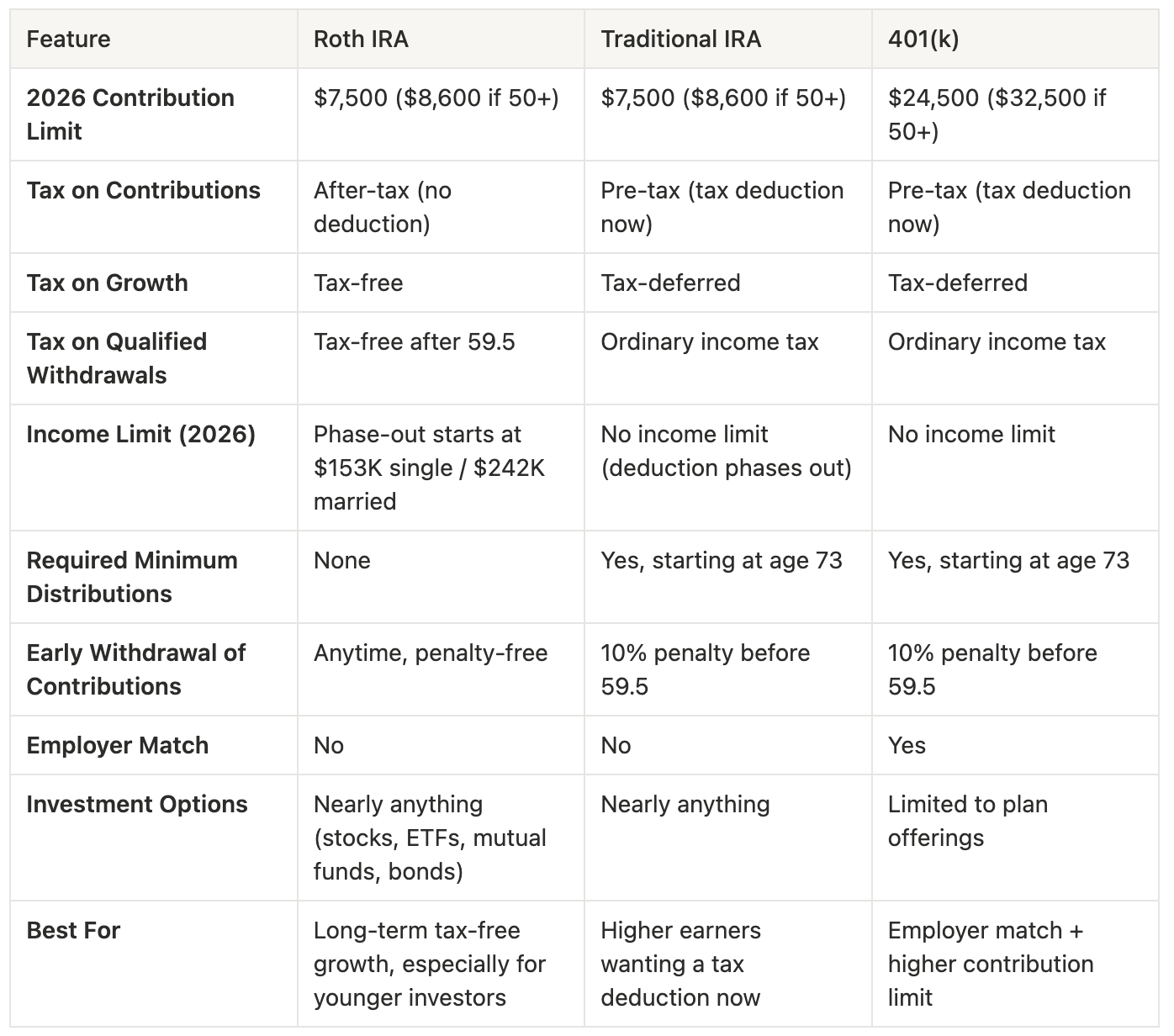

Comparison Table

Who is this for?

Anyone with earned income who wants tax-free growth and tax-free withdrawals in retirement

Investors under 50 who expect their income and tax bracket to be higher in the future than it is today

People who want more investment flexibility than a 401(k) offers

Anyone who has already captured their full 401(k) employer match and is looking for the next step

Individuals earning below the 2026 Roth IRA income limits ($153,000 single / $242,000 married filing jointly)

FAQ

How is a Roth IRA different from a savings account?

A savings account holds cash and earns interest (currently 4–5% in high-yield accounts). A Roth IRA is an investment account — your money goes into stocks, index funds, or ETFs that have historically returned 8–10% annually over long periods. A Roth IRA is for long-term wealth building. A savings account is for short-term needs and emergencies.

What if I make too much money for a Roth IRA?

If your income exceeds the phase-out range ($153,000–$168,000 single in 2026), you can use a backdoor Roth IRA strategy. This involves contributing to a traditional IRA and then converting to a Roth. It is a widely used, legal strategy supported by most major brokerages. Consult a tax professional to ensure proper execution.

Should I choose a Roth IRA or a 401(k) first?

In most cases, capture your 401(k) employer match first — the match provides an immediate 50–100% return on your contribution. After securing the match, fund your Roth IRA for its tax-free growth and broader investment options. Then go back and increase 401(k) contributions if budget allows.

Can I withdraw my contributions early?

Yes. Roth IRA contributions (not earnings) can be withdrawn at any time without taxes or penalties. Earnings withdrawn before age 59.5 may be subject to taxes and a 10% penalty unless an exception applies. For long-term investors, the goal is to leave the money invested.

What happens if the market drops after I invest?

Market declines are a normal part of investing. Based on historical data, the S&P 500 has recovered from every major decline, though recovery timelines vary. For investors with a 20–30+ year horizon, downturns have historically represented buying opportunities — more shares purchased at lower prices. The risk is in selling during a downturn, not in the downturn itself.

What's the difference between a Roth IRA and a Roth 401(k)?

Both offer tax-free growth and withdrawals. A Roth 401(k) is offered through your employer with a higher contribution limit ($24,500 in 2026) but limited investment options. A Roth IRA is opened individually with a lower limit ($7,500) but full investment flexibility. If your employer offers a Roth 401(k) match, you can use both.

Sources

All content is for educational purposes only. Investing carries risk and past performance does not guarantee future results. This is not investing advice, specific recommendations, or legal advice. Consult a qualified professional for guidance specific to your situation.