The Order of Investing: Where to Put Your Money First

The order of investing is a prioritized sequence for where to direct your money to maximize tax advantages, employer benefits, and long-term growth. It applies to anyone with earned income who wants to build wealth systematically, whether you're investing $100/month or $5,000/month. Getting the order right matters because each account type offers different tax treatment, and funding them in the wrong sequence can cost you tens of thousands of dollars over a career.

TL;DR

Start by contributing enough to your 401(k) to capture your full employer match. Next, fund a Roth IRA ($7,500/year in 2026) invested in a low-cost S&P 500 or total market index fund. After that, increase your 401(k) contributions toward the $24,500 annual limit. Once tax-advantaged accounts are funded, open a taxable brokerage account for additional investing. Maintain a 3–6 month emergency fund in a high-yield savings account throughout. The order maximizes tax benefits at each stage. Automate contributions so the system runs without daily decisions.

The Framework

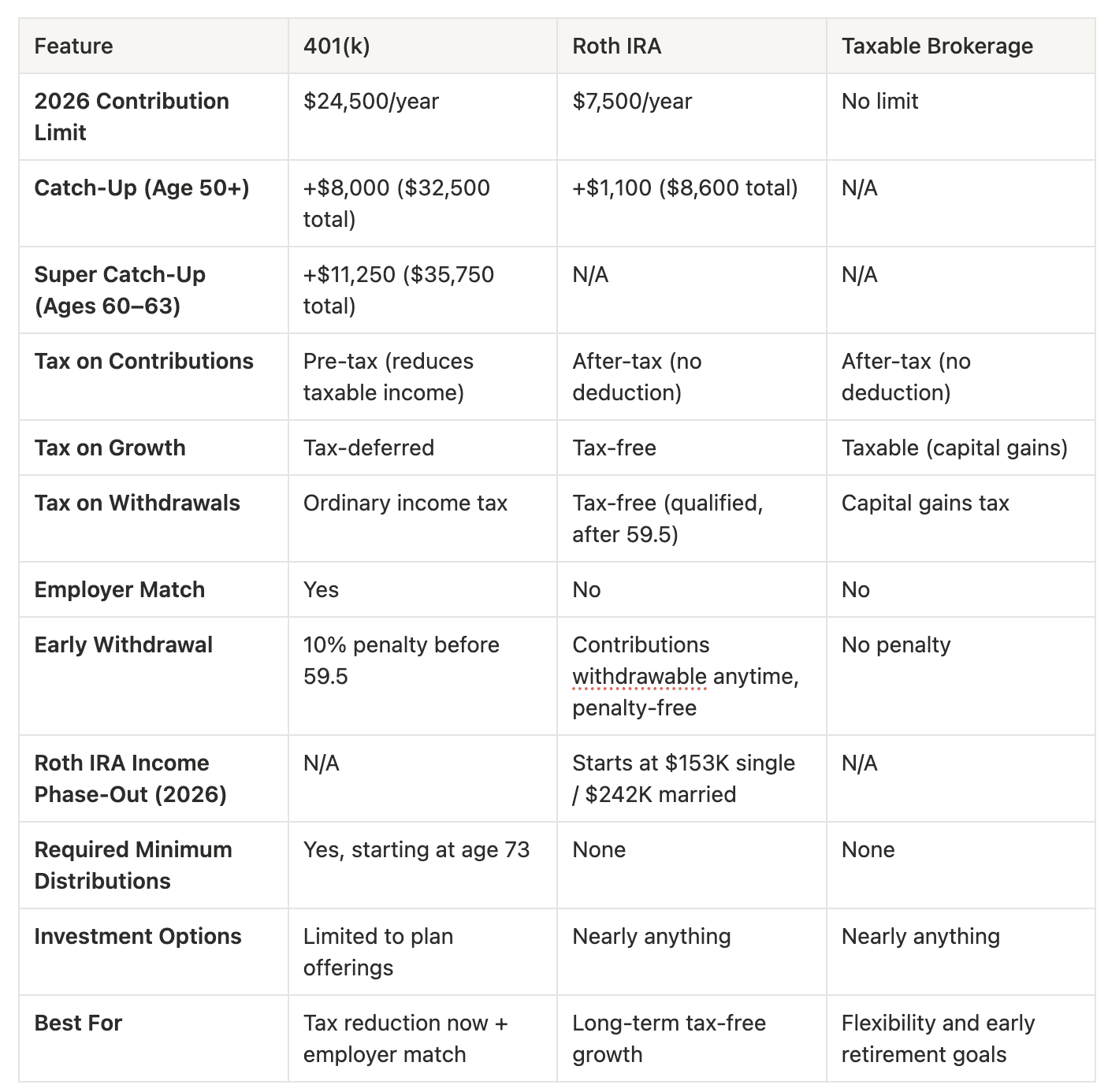

Capture your 401(k) employer match. If your employer matches 4% of your salary, contribute at least 4%. An employer match is a 50–100% immediate return on your contribution, depending on the match formula. No other investment vehicle offers a comparable guaranteed return. (IRS: 401(k) 2026 limits)

Max your Roth IRA. The 2026 limit is $7,500 ($8,600 if you're 50+). That's $625/month. Pick one index fund, VOO, VTI, or FXAIX. Contributions grow tax-free and qualified withdrawals in retirement are tax-free. For most people under 50, the Roth IRA is the most tax-efficient growth vehicle available. (IRS: IRA contribution limits)

Increase your 401(k) toward the max. The 2026 employee deferral limit is $24,500. If you're 50+, the catch-up contribution is $8,000 ($32,500 total). Ages 60–63 qualify for the SECURE 2.0 "super catch-up" of $11,250 ($35,750 total). Every dollar contributed reduces your taxable income for the year.

Open a taxable brokerage account. No contribution limits. No withdrawal penalties. No age restrictions. Same index funds. This account provides flexibility for goals before age 59.5, like early retirement, a down payment, or supplemental income.

Maintain your emergency fund. Keep 3–6 months of essential expenses in a high-yield savings account earning 4–5% APY. This is not an investment, it's a buffer that prevents you from selling investments or taking on debt during an unexpected expense.

Comparison Table

Who is this for?

Anyone with earned income who wants a clear, prioritized system for where to invest

Beginners who feel overwhelmed by the number of account types available

People currently investing but unsure if they're funding the right accounts in the right order

Households earning under $153K (single) or $242K (married) who qualify for direct Roth IRA contributions

Workers with an employer-sponsored 401(k), especially those with an employer match they haven't fully captured

What Changed in 2026

401(k) limit increased $1,000 — from $23,500 to $24,500 (IRS Notice 2025-67)

Roth IRA limit increased $500 — from $7,000 to $7,500

Roth IRA income phase-out raised — single filers: $153,000–$168,000 (up from $150,000–$165,000). Married filing jointly: $242,000–$252,000 (up from $236,000–$246,000)

50+ catch-up contributions increased — 401(k) catch-up: $8,000 (up from $7,500). IRA catch-up: $1,100 (up from $1,000)

Mandatory Roth catch-up rule takes effect January 1, 2026 — If you're 50+ and earned over $150,000 in FICA wages the prior year, catch-up contributions to your 401(k) must be made on a Roth (after-tax) basis. Pre-tax catch-ups are no longer available for high earners. This is a SECURE 2.0 provision.

Super catch-up for ages 60–63 continues — An additional $11,250 catch-up (instead of the standard $8,000), bringing the total 401(k) limit to $35,750 for those in this age window

FAQ

What if my employer doesn't offer a 401(k) match?

Skip to the Roth IRA as Step 1. If your employer offers a 401(k) without a match, you can still use it for the pre-tax deduction — but for most younger investors, the Roth IRA's tax-free growth is typically more valuable when you expect your income to increase over time.

Should I pay off debt before investing?

If you carry high-interest debt (credit cards at 18–25%), prioritize paying that down. The effective return on eliminating a 22% interest rate is difficult to match with market investments. However, contributing enough to capture your full employer match is still worth doing simultaneously — the match provides an immediate 50–100% return.

How much should I invest per month?

A common target is 20–25% of gross income across all investment accounts. If that's not realistic right now, start with whatever you can. $100/month invested from age 25 to 65 at a 10% average annual return grows to approximately $632,000. Increase your contributions when your income increases.

What's the difference between VOO, VTI, and VTSAX?

VOO tracks the S&P 500 (approximately 500 large U.S. companies). VTI tracks the total U.S. stock market (approximately 3,600+ companies including mid- and small-cap). VTSAX is the mutual fund equivalent of VTI. Their long-term performance has been closely correlated. Choose one and stay consistent.

What if I can't max out all my accounts?

Most people can't, especially early in their career. Follow the order and fund each step as far as your budget allows. Partial contributions still compound over decades. The priority sequence ensures each dollar goes to the highest-impact account available to you.

What's the mandatory Roth catch-up rule starting in 2026?

Under SECURE 2.0, employees age 50+ who earned over $150,000 in FICA wages in the prior year must now make 401(k) catch-up contributions on a Roth (after-tax) basis. This means you pay taxes on those contributions now, but the growth and future withdrawals are tax-free. Employees earning under $150,000 can still choose pre-tax or Roth for catch-ups.

What's the super catch-up for ages 60–63?

SECURE 2.0 created a higher catch-up limit for people aged 60 through 63. Instead of the standard $8,000 catch-up, this group can contribute an additional $11,250 — bringing the total 401(k) limit to $35,750 in 2026. This is a four-year window designed to accelerate retirement savings for people approaching retirement.

What if I make too much for a Roth IRA?

If your income exceeds the phase-out range ($153,000–$168,000 for single filers in 2026), you can use a backdoor Roth IRA. This involves contributing to a traditional IRA and then converting it to a Roth. It's a widely used strategy, and most major brokerages support it. Consult a tax professional to ensure it's executed correctly for your situation.

Sources

All content is for educational purposes only. Investing carries risk and past performance does not guarantee future results. This is not investing advice, specific recommendations, or legal advice. Consult a qualified professional for guidance specific to your situation.